De pagina ververst bij het selecteren van een onderwerp.

Sla artikel navigatie over.ARC Fund Risk Management Framework

The Fund Manager applies a Risk Management Framework to identify, measure, manage, monitor and report risks, and sets the corresponding risk indicators, limits and risk appetite.

Fraud risks are integrated into this framework, as fraud is considered an inherent operational risk that may lead to financial loss or reputational damage. Industry standards highlight that fraud may arise where opportunity, pressure and rationalization converge, underscoring the need for robust preventative and detective measures. To mitigate these risks, internal and external fraud risks are addressed through a system of internal controls embedded in daily processes, including segregation of duties, authorization procedures, access controls and automated checks.

The Fund’s risk management structure is staffed by the Director Finance & Risk and the Risk and Compliance Officer. In addition, Amvest is subject to an independent ISAE‑based assurance framework. Under ISAE 3402 key processes and controls are annually tested by an external auditor to assess design and operational effectiveness.

During the reporting period, no instances of fraud with a material impact on the Fund were identified.

Every quarter, or more frequently in case of significant events, the defined risk categories are assessed in close consultation with the Portfolio Manager. Findings are reported in the quarterly Investor Report’s Risk Management Dashboard. The Director Finance & Risk is responsible for reporting to all relevant stakeholders.

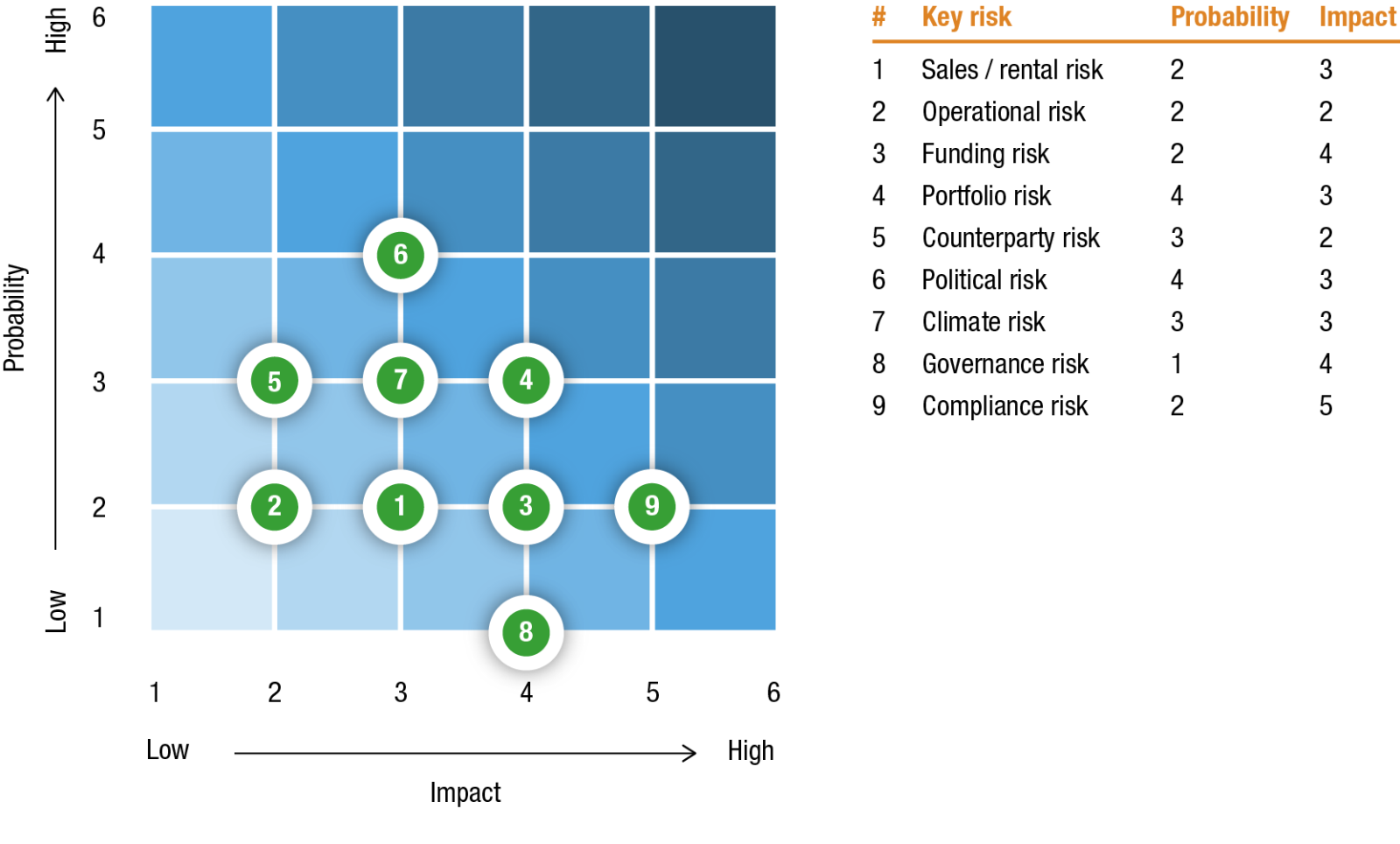

Identified risks of the ARC Fund

-

Sales / rental risk: the risk that a home or a property cannot be sold / rented out within the envisaged period at the targeted sales / rental price.

-

Operational risk: the risk resulting from inadequate or failed operational processes and/or systems.

-

Funding risk: the risk of funding shortages and mismatches between funding and commitments because the ARC Fund:

-

-

is unable to timely fund its commitments with new or existing equity and/or debt commitments at the desired conditions and/or from divestment proceeds;

-

is in breach of its contractual obligations for its debt funding, which results in defaults and mandatory repayments; or

-

incurs short-term liquidity shortages due to the insufficient coordination (by timing and amount) of cash inflows and outflows.

-

-

Portfolio risk: the risk that the portfolio development and operational results are not in line with the Portfolio Plan, and, as a result, targeted returns are not achieved.

-

Counterparty risk: the risk that a counterparty fails to fulfil contractual or other agreed upon obligations. The main counterparties for the ARC Fund are Investors, banks, developers, appraisers, property managers, tenants and buyers. The risk of concentration of counterparty exposure is also reflected under counterparty risk.

-

Political risk: the risk that policy changes and regulations by (local) authorities or governmental bodies affect the strategic objectives and business of the ARC Fund. The real estate sector increasingly experiences negative consequences from external constraints linked to policy, such as utility grid congestion and nitrogen emission limits. The constraints may lead to delays in the completion and start of operation of new projects. Although the contractual performance risk lies with the developer, any potential negative impact for the ARC Fund increases the overall political risk.

-

Climate risk: the risk that the ARC Fund is not adequately adapting to constraints resulting from climate change, climate policy, climate adaption strategy and/or fails to adequately report on its actions to address climate change.

-

Governance risk: the risk that a conflict of interest is not adequately addressed by means of governance as well as checks and balances, and/or the risk that the ARC Fund is inadequately equipped to operate in the event of a conflict of interest.

-

Compliance risk: the risk that the ARC Fund and its operation are in breach of legislation and regulations, which may jeopardise the Fund’s AIF status.

Risk appetite and evaluation 2025

The ARC Fund invests in income-producing real estate investments in the Dutch residential sector. The generated returns from rental income are relatively stable, and the ARC Fund acquires new projects on a turnkey basis, without incurring development risk. The ARC Fund uses modest levels of leverage to enhance returns. In line with its INREV core fund risk profile, the ARC Fund has a relatively low-risk profile and correspondingly low-risk appetite.

The potential adverse economic impact of rent regulation and the ongoing legal uncertainty regarding the fairness of rent indexation clauses received particular attention. Four quarterly risk meetings were held to discuss development of risk indicators together with the Director Finance & Risk, the Portfolio Manager and the RCO. The potential adverse economic impact of increasing rent regulation and counterparty risk on selective projects received special attention. So far, the adverse impact of expanding rent regulation on the Fund’s performance has been limited.

Sales/Rental risk

The sales/rental risk remained stable due to the increase in investment market activity and volume, as well as the high demand for individual sales. Vacancy levels in the portfolio remained at low levels throughout 2025.

Political risk

Changes in (local) legislation, designed to interfere in the residential investment market or which limit the feasibility of new projects, may impact the ARC Fund’s ability to execute its strategy. The Dutch government and local authorities implemented a new rent regulation in 2024 which impacted the rental growth capacity of the ARC Fund in 2025 for select assets.

Counterparty risk

The counterparty risk remained stable compared to 2024, as the Fund’s pipeline exposure to construction and development companies decreased further due to successful completion of a number of projects. The sale of a non-strategic asset was delayed during 2025 and closed only in December 2025. One project increased counterparty risk due to a defaulting contractor, which can potentially lead to delays for completion. We continued to manage this risk effectively with no material defaults occurring.

Portfolio risk

The portfolio risk remained stable compared to 2024. The Fund’s direct return performance benefited from lower operating costs, while indirect return was driven by a second year of continued positive valuation trend. The targets for asset rotation strategy were achieved at commercially feasible levels. The dividend yield percentage is declining, due to increasing portfolio valuation as well as not achieving the individual sales target in terms of volume and profit margin.

Funding risk

During 2025, the debt diversification and refinancing programme was successfully completed. In addition, the ARC Fund completed the execution of its debt funding strategy with its second green bonds issuance. All refinancing risks are addressed until at least January 2029. The €450 million revolving credit facility remains fully undrawn and provides solid funding flexibility.

The Fund made use of sales proceeds and new equity inflow to fund its project pipeline and redeem participations.

€96 million equity commitments were drawn in 2025. €197 million of new equity commitment was sourced at the end of the year, which is partially being used for capital redemptions in first quarter of 2026. On balance, the overall funding position improved during 2025, and funding risk therefore decreased further.

Various scenarios for liquidity – covering the expected realisation time of the acquisition pipeline and going beyond the current Portfolio Plan horizon of 2026 – were calculated and monitored. No liquidity constraints occurred in 2025 or are expected in 2026. The ARC Fund plans to secure new equity in 2026 (subject to market conditions) to fulfil outstanding redemption requests as well as fund and grow its pipeline in the coming years.

Compliance risk

Due to the fiscally transparent status of the Fund, the ARC Fund is not able to incur any form of development risk as part of the acquisition of new projects for its pipeline. Therefore, the ARC Fund acquires its projects on a fixed-price, turn-key basis. In certain situations, the ARC Fund is able to secure a fixed-price, turn-key project subject to final permits and planning prior to the start of construction. In these cases, the ARC Fund will obtain a put-option with a longstop date from the third-party developer, in order to be able to unwind the transaction in the event that permits or planning might not be obtained within an agreed time frame. During 2025, no contracts that are subject to put options were entered into by the Fund.

Between 2023 and 2024, several Dutch administrative courts ruled in individual rental dispute cases that rent indexation clauses in liberalised housing — specifically clauses allowing rent increases above CPI — may, in certain circumstances, conflict with the requirements of European Directive 93/13/EEC on unfair terms in consumer contracts. These rulings created sector wide uncertainty regarding the enforceability of indexation and surcharge clauses. On 29 November 2024, the Dutch Supreme Court provided important clarification. The Court ruled that the elements of rent adjustment clauses must be assessed separately: the inflation linked indexation component and any surcharge on top of CPI serve different purposes and should not automatically be treated as one. The Court held that an annual surcharge of up to 3% above CPI is generally not considered unfair, and such clauses may enhance contractual transparency by providing clarity on future rent increases. This significantly reduced both the probability and potential impact of non-compliance risks related to existing rental contracts. However, in Q4 2025, a Dutch administrative court announced its intention to re-examine rent indexation clauses and to submit new preliminary questions to the European Court of Justice on this topic. This re-opened regulatory uncertainty, as the potential scope, timing and impact of any future European Court interpretation remain unknown. Internal risk reporting (e.g., quarterly fund reporting) reflects this development as a low probability but high-impact scenario.

The Fund continues to monitor legal developments, maintain a prudent rent adjustment policy and evaluate the need for mitigating measures should the legal framework evolve.

Overall risk performance

Management has performed its risk assessments in 2025 and concluded none of the risk limits set by the Fund Manager for the defined risk categories were exceeded.

Updated Risk Management Framework

The ARC Fund’s Risk Management Framework is a dynamic framework. The Fund Manager assesses, monitors and reviews the risk management function, policy, framework and its risk appetite, indicators and limits on an annual basis and reports on these matters to the Advisory Board and Investors of the ARC Fund.

If necessary, the Fund Manager adjusts previously described risk categories in close consultation with the RCO and its stakeholders.

Figure 26 plots the risk categories on an impact/ probability axis.

Figure 26: Plotted risk (impact/probability)